By Gabriel Temporal, Nicholas Ribeiro, Diana Viotti and Rafael Freire

- Billing Rules are tools for planning and formalizing the collection actions that an organization must implement to recover overdue amounts.

- The aim is to minimize delinquency and mitigate the use of resources used to carry out these measures, in a preventive, corrective or coercive manner.

- In other words, the Billing Rules can be understood as a set of well-defined steps and activities that the company will adopt, following a pre-established cadence, to approach its customers at different points in the payment cycle.

In the article that began this series of publications on Billing Management and Order To Cash, we covered the nine main good market practices associated with the subject. In fact, if you have not had the chance to read it yet, we recommend that you do so before reading this article – it holds a wealth of information that provides a good introduction to the subject covered here.

Among the strategies discussed, we introduced the reader to billing rules, presenting the most applied macro-steps and suggesting general recommendations for implementing the method. Also in this last article, we mentioned that there are several separate ways of structuring a good dunning rule, depending on the context and characteristics of the organization. For example, for collection actions to be more effective, it is necessary to define the most proper strategy for each debtor profile and each type of debt, as well as considering the different contexts and possible scenarios in which the process could unfold.

To delve deeper into the subject, this second article aims to explore it in more detail. Here, we will discuss the basic concepts and main benefits of the ruler, as well as detailing the step-by-step process for implementing it in your company. Finally, we will also bring you trench tips and real-life success stories to show how to really apply these recommendations into your business.

What is the Billing Rule?

It is an instrument for planning and formalizing the billing actions that an organization must put into practice to recover overdue amounts – payments owed by its customers or other external factors that are in arrears – in a systematic and structured way. The aim is to minimize delinquency and rationalize the use of the resources employed in carrying out these measures, in a preventive, corrective or coercive way.

In other words, the Billing Rule can be understood as a set of well-defined steps and activities that the company will adopt, following a pre-established cadence, to approach its customers at different points in the payment cycle and through different communication channels. The aim is to recover credit and regularize the situation of those whose payments are overdue.

In this context, communication is naturally a key aspect in increasing the chances of successful collection actions. It must be clear and assertive, while at the same time professional and respectful to preserve the bond with the customer and avoid escalating possible friction.

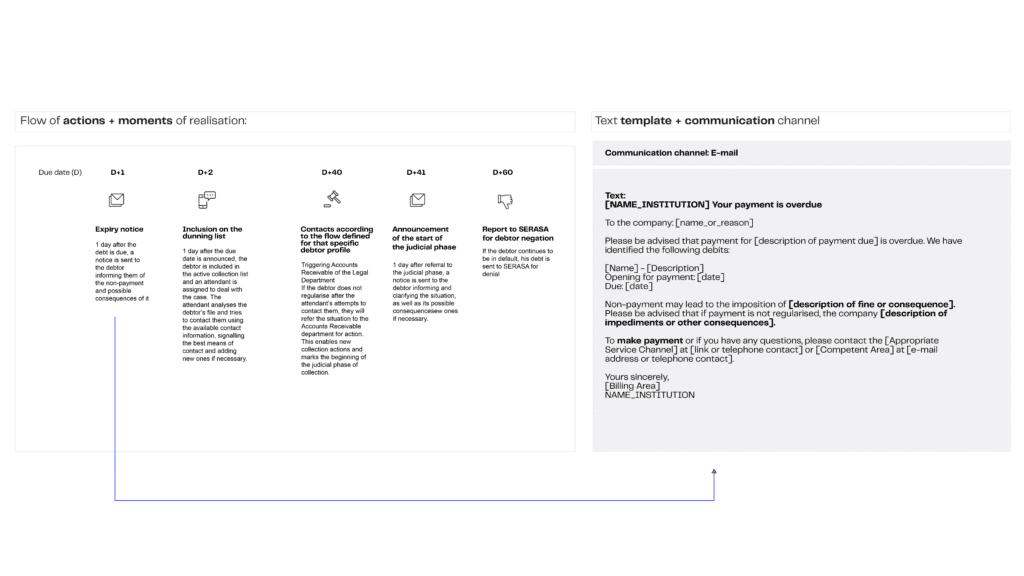

To make it easier to understand and help make the idea discussed in the article tangible, we will show you an illustrative example of applying the billing rule below. Note that the image shows a hypothetical flow of actions with a sign of when each one should take place, as well as a text template to be used to send the e-mail on D+1, this being the communication channel chosen for the first contact.

As can be seen above, the image reflects some fundamental attributes that every well-implemented rule has, such as:

- Who: To which debtor profile and/or business process is the billing action directed?

- What: What types of communication and through which channels can collections be carried out?

- When: What is the timing and order of the collection actions to be carried out?

- How: Seeing the principles of behavioral design, how will the “tone” of the communications escalate in severity over time?

Finally, we must emphasize one more key aspect for the successful implementation of this strategy: the automation of the billing rules. Good market practice proves the adoption of a Pareto rule so that most of the actions provided for in the rule are automated and only a residual part is done with human effort. This perspective radically changes the premises of the work and directs the construction of the rules towards scaling the value generation of this practice.

Benefits of the Billing Rule

Adopting the Billing Rule as a strategy generates a series of advantages. Despite the challenges involved in its planning and implementation, the tool enables remarkable results, capable of positively affecting the business and raising the maturity level of your organization’s Order To Cash process.

We highlight four of the main benefits generated by adopting the Rule:

- Greater efficiency in credit recovery: The organization and systematization of collection actions provide a significant increase in the chances of success in recovering overdue amounts. This is because each stage of the Rule is carefully planned so that, regardless of the context, it is as appropriate as possible for achieving the goal of reducing the level of customer default;

- Optimization of the Collection team’s efforts: By implementing a more focused and intelligent collection approach, based on well-defined and standardized stages, as well as prioritizing the most relevant cases, the adoption of the Rule optimizes the use of resources and allows the Collection team to act more strategically. Ultimately, greater efficiency in the execution of the process also leads to a potential reduction in the operating costs involved;

- Preservation of the customer relationship: By adopting respectful, empathetic, clear and professional communication in every small interaction with the customer, as proposed in this article, the risks of collection actions negatively affecting the relationship with the debtor customer are reduced. In addition, this strategy also helps to keep a positive image of the company and increases the chances that, even in future situations of default, the customer will feel valued and understand the importance of the financial commitment, which contributes to future business opportunities; and

- Reducing the need for coercive measures: As is already well known, the main objective of the Billing Rule is to resolve cases of default quickly and amicably. This means that a well-structured Rule can avoid the need for coercive measures, such as legal action, which generate additional stress and costs, as well as time uncertainties. To achieve this, a gradual approach allows the company to begin collection actions through friendlier contacts and reminders in a conciliatory tone, which – progressively – open opportunities for the customer to regularize their situation in a friendly manner. If this does not happen, there is a natural progression to more coercive measures – but only in atypical, one-off cases.

Implementation steps

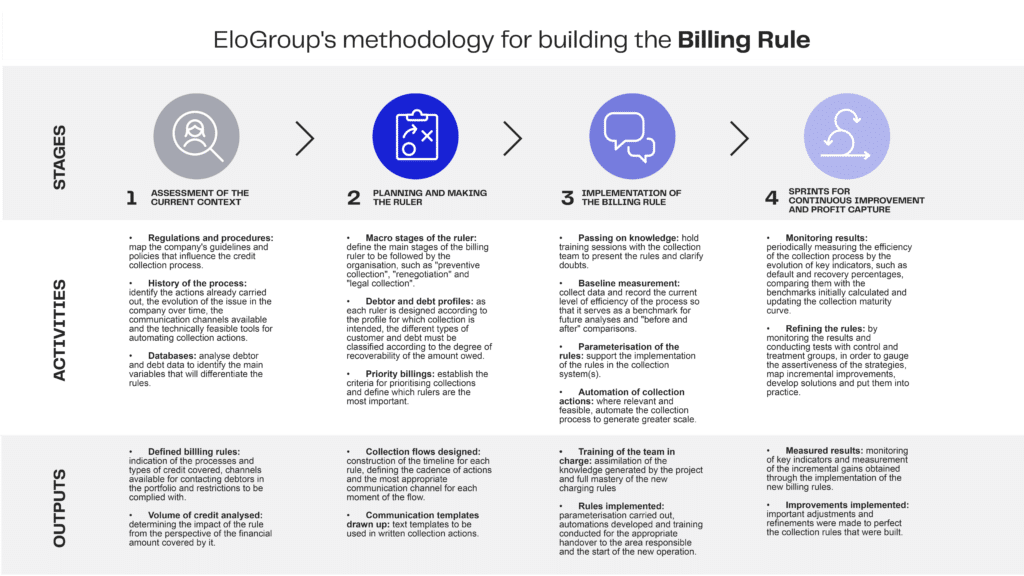

Once we have clarified the concept and the main benefits of the Billing Rule, we can move on to the step-by-step process that allows you to implement this strategy in your company. Based on the method developed by EloGroup, the implementation process can be summarized in four main stages, as illustrated and detailed below. We recommend that you enlarge the image, or open it in a new tab, to analyze the information presented more easily.

Trench tips

To complement the proposed method, some practical recommendations are interesting for maximizing the results generated and reducing possible obstacles in implementing the strategy. Below are ten trench tips associated with the construction of billing rules, based on our experience in real-life situations:

1 – Communication Channels: the contact with customers can take place via a wide variety of channels, such as telephone, email, SMS, online customer service portal, instant messaging apps, push notifications in apps, pre-recorded voice calls or even social media. Choosing the right communication channel to carry out your collection actions will depend heavily on the type of strategy chosen, since this defines the degree of effectiveness desired and the level of effort the company is willing to put in;

2 – Customer preferences: in line with the definition of the communication channel to be used, it is essential that the company also considers how the customer himself accepts being summoned and/or charged, to avoid friction and even legal proceedings. For example, the issue of “vexatious billing” is a recurring one in the courts and the jurisprudence tends to be in favor of the debtor. In order to do this, it is first necessary to collect these preferences from customers and form a database to use the information. Ultimately, the aim is to minimize risks and ensure full adherence to current policies, regulations and laws;

3 – Adoption of Behavioral Design Principles: in general, any communication set up between a company and its customer should have its foundations in the field of Behavioral Design. This area studies how people act and feel when faced with certain stimuli, using these perceptions to make the process simpler and more effective. In the context of billing, this knowledge base helps define the most proper tone for each message and the feeling to be induced in each communication, as shown below;

| BILLING TIME | STRATEGY | RECOMMENDED POSTURE | STIMULATED FEELING |

|---|---|---|---|

|

Before due |

Sending reminders |

Friendly and helpful |

Positive, with the prospect of avoiding delay |

|

Recent due |

Regularization stimuli |

Conciliatory and guiding |

Slight discomfort, but still with the prospect of regularization soon |

|

After due |

Recuperation attempt |

Coercive and respectful |

Discomfort based on awareness of the delay and the associated consequences |

4 – Rule specialization: good market practice recommends defining a limited number of rules and designing them according to the main borrower and debt profiles. In practice, the ideal is to have portfolios that justify the existence of a rule on their own or that can run as a spin-off from a standard rule to reduce the level of complexity involved. This makes it clear that it is not a question of designing multiple rules for all types of clients in a misguided attempt to increase the value generated by this practice. In fact, the enormous potential of the billing rule lies precisely in being specific to a particular niche and in aiming for a balance between the collection effort and the degree of debt recoverability;

5 – Standardization of Actions: for each rule, a communication standard should be established to be followed by the entire team responsible. This improves consistency in interactions with debtors and avoids undesirable lack of control in approaches. A good example is the use of standardized written messages to speed up and standardize the execution of the process. It’s also worth emphasizing that when drawing up these templates it is essential to adopt the principles of Communication Design to increase the chances of success of the actions taken, such as ensuring clarity in the writing of the message and generating an assertive “call to action” for the debt to be paid;

6 – Preventive Billing: although the discussion of billing rules has a strong tendency to deal with cases of customers already in default, the real success of this strategy lies in preventing default in a preventive manner. This involves a meaningful change in the organization’s culture and mindset, so that it understands that the focus is on reducing defaults from occurring in the first place, even though the level of recovery is also being seen, as this is a key collection indicator;

7 – Massive vs. Personalized billing: another important tip concerns precision in the choice of collection approach to balance the level of effort and resources used depending on elements such as the organization’s context, the size of the team responsible, the average debt ticket and the percentage of defaults. In this context, a mass strategy benefits greatly from the automation of billing actions and the adoption of Behavioral Design principles, which help induce specific behaviors from the target audience. On the other hand, a personalized approach makes it possible to adapt the available tools according to the characteristics of each client and thus increases the chances of success. For example, customers who find it difficult to organize their financial obligations, or who regularly fall behind on payments, can respond positively to reminders sent just before the debt is due, which help them keep their bills up to date and avoid interest and fines;

8 – Renegotiation and BATNA: intrinsic to collections management, renegotiating overdue debts is a strategy that should always be considered. To do this, it is essential to have well-defined and standardized procedures that clearly establish the “rules of the game”. As a result, the team responsible can conduct the process properly, even in different negotiation scenarios. It also creates greater transparency about the terms and conditions of the renegotiation, as well as ensuring fair and consistent treatment between multiple clients.

Even in this context, the concept of BATNA (Best Alternative To a Negotiated Agreement) can also be particularly useful. This is a clear definition of the best option available to the company when it is not possible to reach an agreement with the defaulting customer. In other words, it is the alternative that the company considers most helpful, or least damaging, compared to the scenario in which there is no agreement – for example, accepting a partial debt repayment plan or a renegotiation of terms, even if it is not ideal. Clarity about BATNA helps the company to set up its negotiating limits and, on that basis, make more informed decisions about the conditions and agreements it is willing to accept or not.

9 – Debt Outsourcing and Securitization: as part of every rule, it is expected that there will always be a residual amount of debt whose value to be recovered will not compensate for the effort made. In these cases, it is recommended to adopt the strategies of “billing outsourcing” and/or “debt securitization”, both of which were mentioned as good practices in the first article in this series. The central idea here is to pass on amounts considered unrecoverable by the company and then focus human efforts on cases with a better prognosis, guaranteeing an efficient and more strategic approach to credit recovery; and

10 – Testing and continuous learning: finally, we would also like to emphasize conducting A/B tests as part of the process of continuously improving collection rules. The recommendation is to show at least one treatment and control group for each analysis conducted, in addition to defining statistically significant samples – there are several free websites that can help you with this calculation. As a result, it is possible to find any random effects that affect the results, reduce existing confirmation biases and, above all, mitigate the risk associated with the large-scale implementation of charging actions.

EloGroup Success Stories

Finally, we bring you two cases of consultancy projects carried out by EloGroup, in which expertise in the application of the Billing Rule was central to the success of the results.

CASE 1: Design of a new credit management model for a financial institution

Challenge:

Build a new Credit Management model for a state-owned financial institution capable of:

- Promote greater compliance;

- Reduce financial losses; and

- Increase agility and operational efficiency in credit management.

Macro activities:

- We plan the sequence of activities, consolidate the desired vision of the future and draw up a work plan;

- By immersing ourselves in critical processes and finding the main opportunities for improvement, we built a diagnosis of the institution’s current situation; and

- Based on the outputs of this assessment, we designed the new Credit Management model which, in turn, was implemented by carrying out the actions detailed in the implementation plan.

Application of the Billing Rule:

Among the elements of Credit Management pointed out by the diagnosis as challenges, the billing mechanisms stand out. To structure efficient rules, detailed work was carried out to analyze customer and debt profiles. In the end, it was agreed to create six different rules, focused on the main debtor profiles and with a common primary guideline of intensifying collection in the first few days of default.

Main results:

By adopting the rules, together with the definition of performance targets and daily monitoring of results, it was possible to:

- Increase the execution of billing events from 45% to 96%;

- Reduce the overall default rate by 56%;

- Reduce by 20 per cent the default indicator between 15 and 89 days overdue;

- Shorten the average renegotiation time from 70 to 21 calendar days; and

- Increase the average number of renegotiation agreements per month by 3x.

CASE 2: Improving the billing process at a state secretariat

Challenge:

To increase the effectiveness of the collection process carried out by the Secretariat based on a set of analyses and to support the implementation of best market practices.

Macro activities:

The project covered the regulatory, process and technological aspects of billing.

- It began with a situational diagnosis of the current Billing Model and the classification of the Billing Portfolio – also known as the “Rating”; and

- Based on this assessment, the new administrative billing method was designed, with proposals for actions to improve registration, new legal collection tools and mechanisms, as well as adjustments to the organizational structure of the areas involved and details of the skills needed to operate the new method.

Application of the Collection Ruler:

As a central part of the new methodology, seven billing rules were built, as well as a strategic dashboard that centralizes the main indicators relating to the use and effectiveness of these portfolios.

Main Results:

The new billing method adopted made it possible to:

- Increase the amount recovered by R$1.8bn – from R$84m in 2020 to R$1.9bn in 2021;

- Enable more than 413,000 collection communications between 2020 and 2021, corresponding to a total volume of R$11.1 billion in amounts owed;

- Achieve a 17.1% rate of return on collections; and

- Gaining maturity in 20 collection practices, out of a total of 56 items assessed.

Conclusion

An effective billing strategy – one that brings productivity and financial benefits to the organization, as well as improving customer relations – is essential in a period of systemic economic challenges. In this context, the implementation of Billing Rules is an essential practice for companies looking to make their operations more efficient and sustainable. The concepts, applications and cases presented in this article show how these Billing Rules can have an objective, expressive and measurable impact that, in the long term, tends to bring even greater gains to the organizations that adopt them.

GABRIEL TEMPORAL works as Senior Consultant at EloGroup.

NICHOLAS RIBEIRO works as Manager at EloGroup.

DIANA VIOTTI works as Senior Consultant at EloGroup.

RAFAEL FREIRE works as Senior Manager at EloGroup.