By Diana Viotti, Gabriel Temporal, Julia Versoni, Nicholas Ribeiro and Rafael Freire

- A Billing Rating is a set of data processing algorithms that distribute debtors or debts into distinct categories of default risk. With the implementation of the Rating, the billing actions that need to be taken are better targeted. For each category adopted, actions can be structured with a friendlier or more coercive approach, depending on the context and customer profile.

- The use of the Billing Rating brings different benefits, such as: differentiation of billing rules, rationalization of the use of resources employed in collection, selective judgment, securitization strategy and input for compliance/relationship programs.

- The implementation process can be summarized in 4 main stages: Understanding and preparation; Exploratory analysis; Modelling and refinement; and Engineering and implementation.

In earlier articles on Collection Management and Order To Cash, we covered the 9 main good market practices associated with the subject and the construction of Billing Rules. If you have not had the chance to read them yet, we recommend that you do so before reading this text, since they provide a wealth of information that introduces the topic of Billing Ratings.

We discussed that it is interesting for billing approaches and actions to be segmented by customer profile and type of debt – so that efforts can be focused and better targeted. One type of segmentation commonly adopted, for example, is based on the risk of default – that is, the likelihood that a certain group of customers will be late with their payments or default on their debts.

Given the complexity and high volume of variables usually involved, this type of segmentation can be done by building analytical models using artificial intelligence. Once developed, these models become extremely useful tools for reducing delinquency and form what is known as a Billing Rating.

To delve deeper into the subject, in this article we will explore the ratings in more detail. We will discuss the basic concepts and the main benefits, as well as detailing the step-by-step process for implementing it in your company. Finally, we will also give you some tips for success.

What is a Debt Billing Rating?

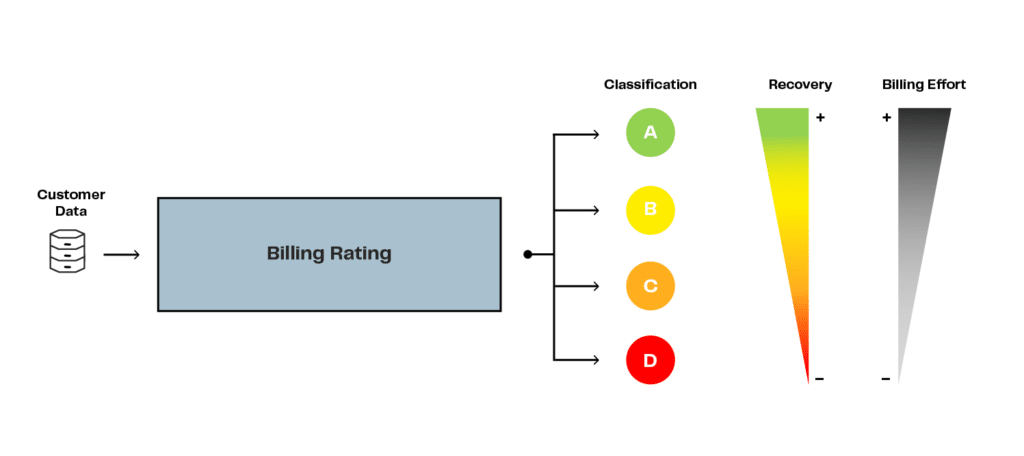

A Billing Rating is a set of data processing algorithms and business rules that distribute debtors or debts into different default risk categories. A rating that classifies debtors tends to be more general but simpler to manage, while a rating that classifies debt tends to be more specific but more complex to manage.

Four risk categories are used, from A to D. In it, category “A” stands for a high probability of debt recovery and “D” represents a low probability of recovery.

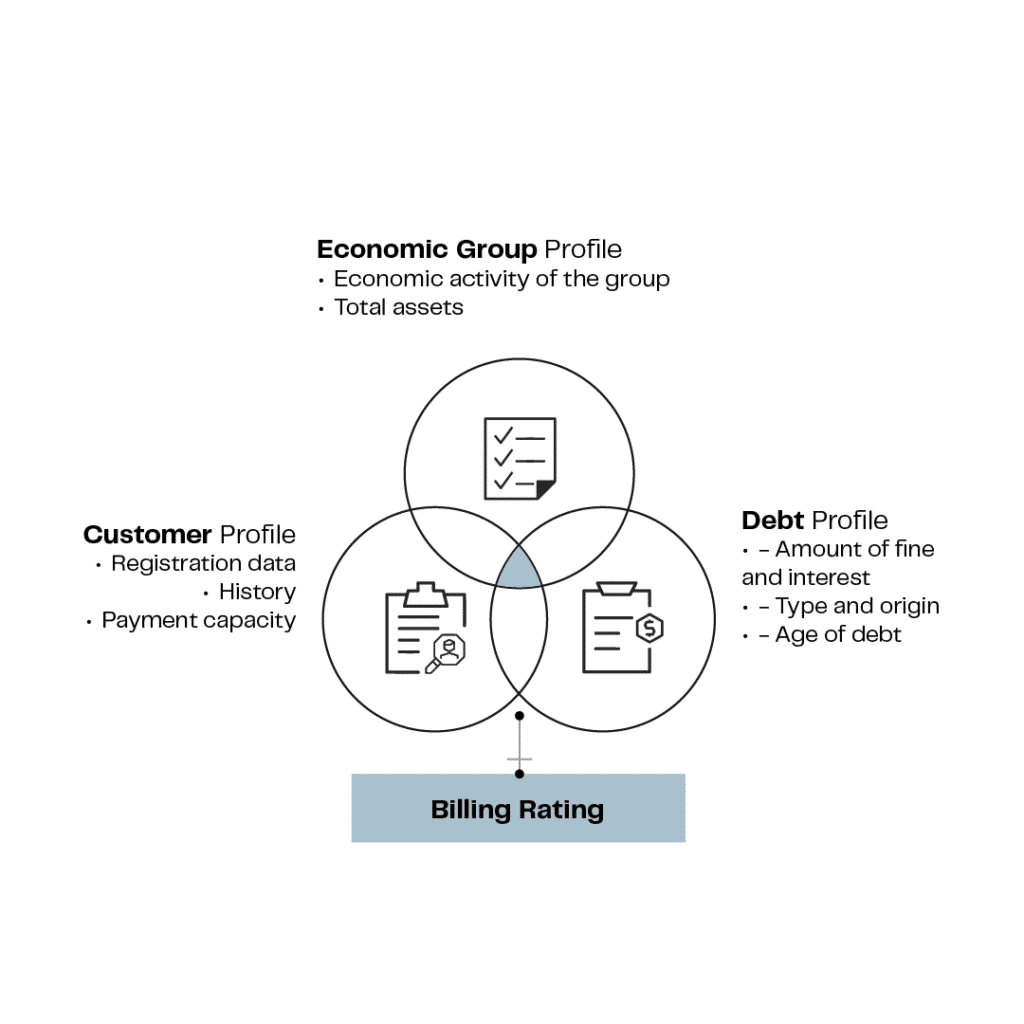

Historical and current data is used to support this segmentation. The data can be obtained internally from the customer’s history with the company or from credit bureaus, for example. Based on this, it is possible to carry out analysis of customer payment behavior and default patterns.

Among the construction of the Rating, three main dimensions of the debt are considered, them being:

These dimensions are incorporated into the algorithm as criteria/guidelines for selecting the variables that will be used for the rating. In addition, when building the Rating model, Business Rules can be used to classify debtors, as well as statistical and Machine Learning algorithms. This is because the use of business rules has lower costs and shorter development and implementation times, as well as greater interpretability of the rating obtained.

The figure below shows how a Billing Rating works. In this case, the Business Rules were used as a first filter to refine the data sample that would be interpreted by the Machine Learning model. In this way, it was possible to obtain a more accurate rating solution.

Why implement a Billing Rating?

As we have seen, the Rating makes it possible to classify customers according to their likelihood of recovering the amount owed, and so the collection actions that need to be taken are better targeted. For each category adopted, actions can be structured with a friendlier or more coercive approach, depending on the context and customer profile. As a result, the company’s risk of default is mitigated.

In addition to risk mitigation, we would also highlight other benefits and developments that can be achieved by implementing the model:

- Differentiation of Collection Rulers: Based on the classifications obtained in the Billing Rating, it is possible to structure Billing Rulers for each of them. In this way, a specific collection strategy can be designed for each category, showing what actions and activities should be carried out at each moment and through which channel;

- Rationalization of the use of resources employed in collection: By identifying the level of recoverability of debts, it is possible to direct greater collection efforts towards those with the greatest chance of regularization, which optimizes the use of available collection resources. Also, for debts considered irrecoverable or with a very low probability of recovery, actions can be taken to write off assets and unrecognized accounts, rather than investing resources and energy in their recovery;

- Selective filing: Like the earlier item, by identifying debts that have a lower chance of being settled, it is possible to more accurately target the cases that need to be filed, thus optimizing the necessary collection actions; and

- Input for compliance/relationship programs: A well-constructed Billing Rating can serve as a valuable input for a company’s compliance and relationship programs, as it reflects the company’s ability to manage its risks effectively and keep healthy and secure relationships with its stakeholders. By analyzing the data and results related to the Rating, the company can identify points for improvement, revisit regulations and reinforce certain compliance practices and improve its relationship programs, which potentially contributes to customer satisfaction and loyalty, for example.

How to build a Billing Rating?

Once we have clarified the concept and the main benefits of Billing Rating, we can move on to the step-by-step process that will enable you to adopt this strategy in your company. Based on the method developed by EloGroup, the implementation process can be summarized in 4 main stages, as detailed below.

Understanding and Preparation

The understanding and preparation stage is the time for gathering and understanding the requirements, information and business goals, with the proper collection and preparation of data for analysis. This is the stage in which the availability and quality of the data is assessed, as well as the maturity of the current operation.

Below are some questions to help guide the collection of the necessary information:

- How do you intend to use the rating?

- What data is available?

- Are there any technical, political or legal restrictions to be considered?

- How will the monitoring and handoff of the solution work?

- Who are the approvers?

Exploratory Analysis

Once the first phase has been completed, with sufficient understanding and preparation for the context, the exploratory analysis stage begins, where the focus is on capturing the essential characteristics of the data and preparing the ground for modeling.

In this process, the characteristic that most interests the Rating is the correlation of each variable with the probability of payment for the case analyzed. The main variables considered when calculating Debt Billing Ratings are:

| VARIABLE | DESCRIPTION | RELEVANT INPUTS |

|---|---|---|

|

Registration status |

Use of information available from credit agencies and credit protection agencies to enrich the analysis and obtain the debtor’s credit history. |

Registration data on the debtor company, such as name, address, business ID number, personal ID number, date of foundation or economic act |

|

Payment history |

Analyzing the debtor’s past payment history is important. This includes checking whether there have been any arrears, previous defaults or if the debtor has a solid history of punctual payments. |

Detailed history of the debtor company’s previous payments, including due and payment dates for previous invoices or debts. |

|

Financial capacity |

Assessment of the debtor’s financial health, including its ability to generate sufficient revenue to meet its financial obligations. |

Financial information, like their financial statements (balance sheet, income statement, cash flow), which demonstrate the financial health of the company, its income, expenses, profitability, liquidity. |

|

Debt characteristics |

Evaluation of the terms and conditions of the debt, such as payment period, interest rates and total amount, to better understand the associated risk. |

Specific details about the debt in question (total amount, maturity, interest rates and associated guarantees). |

|

Guarantees and collateral |

Consideration of any assets or collateral provided by the debtor to guarantee payment of the debt, which may affect the credit risk. |

Information on any guarantees or collateral offered by the debtor company to ensure payment of the debt. This may include real estate, equipment, shares, or other forms of collateral. |

|

Characteristics of the debtor’s sector |

Assessing the sector in which the debtor operates is also relevant, as different economic sectors can have various levels of risk. |

Economic prospects, market trends, competition, regulations. |

|

Length of existence of the debtor company |

Companies with a longer history of operation tend to be seen as more stable and reliable than those that are newer to the market. |

Date the company was founded. |

|

Cash flow and indebtedness |

Analysis of the debtor’s ability to generate positive cash flow to meet financial commitments and verification of the debtor’s level of indebtedness in relation to its payment capacity. |

Details on how the debtor company’s cash generation structure, as well as its debt structure, including debt levels in relation to equity and operating cash flow. |

The proper analysis of these variables is fundamental, since when they are incorporated into analytical and statistical models, they will be used to predict debtors’ payment behavior, identify risk patterns and thus inform decisions on collection strategies.

Modeling and Refinement

Next, in the actual modeling phase, different algorithms are explored with the aim of choosing the one best suited to the context in question. As well as building the model itself, it is particularly important to refine it to perfect the model and test variations of the features and parameters defined. The result of these stages is the improved model and the final variables.

We advocate the “methodological sincerity” of assuming that there is no perfect model, i.e. a model that meets all requirements. There will always be a trade-off between aspects of interpretability (i.e. how to explain the weight each variable has on the result and how the model makes its decisions and classifications) and accuracy (how realistically the model is able to predict whether a claim will be paid or not).

When it comes to the choice of Rating modeling method, Classical Programming Models, such as Logistic Regression and SVM, have a higher degree of interpretability, although they may be less accurate. Machine Learning models – like Random Forest, XGBOOST and Neural Networks – on the other hand, can be more accurate than the explanatory power of their results. It is therefore necessary to analyze the advantages and disadvantages of each model to select the one that best suits the needs of each context.

Engineering and Deployment

The engineering stage aims to define the solution’s architecture and put the model into production. At this point, the necessary system integrations will be developed to feed the data, as well as the periodic update routine.

The implementation stage also focuses on updating the organization’s processes and culture to use the new tool. It is important to create procedures for evaluating the effectiveness of the Rating in practice and for supporting the tool.

Success tips

To complement the proposed method, some practical recommendations are interesting for maximizing the results generated and reducing obstacles to implementation. Below are 4 tips for success associated with the construction of Billing Ratings, based on our experience in real situations:

- Ensure data quality: Make sure that the data used to build the model is as accurate and up to date as possible is a determining factor in the quality of the results that the Rating will be able to generate;

- Dedicate the necessary time and care to choosing the most relevant algorithm: It is important that the urgency of having the model implemented does not compromise the attention and care given to selecting an algorithm that really suits that specific context. Once defined, the algorithm will figure out the quality of the Rating. In line with the main current trends, it should also be pointed out that the use of machine learning algorithms can be interesting for improving the accuracy of forecasts, when possible;

- Ensure accessible interpretability: As discussed throughout the article, interpretability is a central element of the model. It is therefore important that the logic and results of the Rating can be justified and understood by all the players involved, so that the criteria used are clear and the tool has the necessary credibility and backing; and

- Onboarding and training the teams: If the Rating is to act as a major driver for classifying customers and debts and for the collection strategies themselves, it is essential that the collection teams are properly trained to understand and use the solution effectively and in compliance with the applicable regulations.

Does your company face collection-related challenges? Do you believe that a dunning rating can help boost your business results? Get in touch with our team!

DIANA VIOTTI works as Senior Consultant at EloGroup.

GABRIEL TEMPORAL works as Case Leader at EloGroup.

JULIA VERSONI works as Consultant at EloGroup.

NICHOLAS RIBEIRO works as Manager at EloGroup.

RAFAEL FREIRE works as Senior Manager at EloGroup.